Global or local? Biopharma’s supply chain challenge

In a letter to doctors on New Year’s Eve, the UK’s chief medical officers made an important point about the Covid-19 vaccination programme: “Vaccine shortage is a reality that cannot be wished away”.1

For the profession, the message was a reminder that challenges were still to come, despite the emergence of multiple vaccines. For biopharma industry observers, meanwhile, the chief medical officers’ warning was a symptom of a perennial issue.

The biopharma industry has grown increasingly dependent on a global supply chain for the manufacturing and distribution of medicines. This has driven cost efficiencies through economies of scale, but it also makes it vulnerable to bottlenecks.

A complex tangle of processes across multiple countries vastly increases the potential for pain points in the biopharma supply chain, and these have knock-on effects that ultimately delay production. In a pandemic, that is both more likely and more catastrophic.

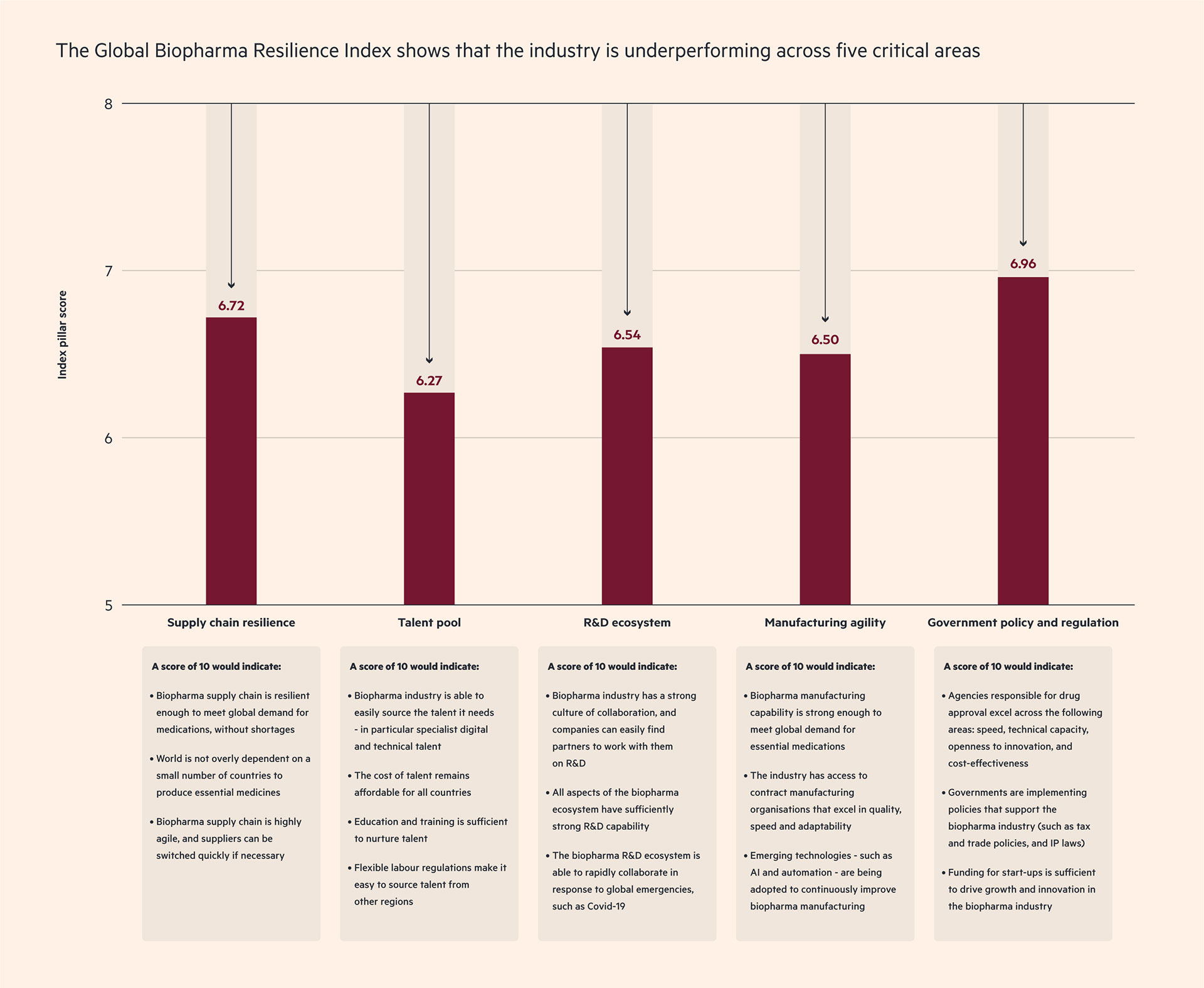

At this critical point, how is the supply chain performing? Findings from Cytiva’s Global Biopharma Resilience Index suggest a mixed picture.

Drug shortages are common

While 50% of executives and policymakers in the survey say their country never experiences shortages of critical medicines such as insulin, this drops to 26% for more specialised areas such as oncology biologics. Respondents from countries with a lower gross national income (GNI) per capita — Indonesia and Thailand, for instance — are more likely to report shortages. For example, 32% of respondents in Indonesia say that their country experiences shortages of oncology biologics more than once a year, compared with none in Switzerland and just 4% in the US.

Meanwhile 51% of executives say that drug shortages increased in their domestic market during the pandemic, although 33% say that the issue had been increasing over the past five years. This points to underlying issues around supply chain resilience, which have been exacerbated — but not caused — by the pandemic.

Part of the problem of supply chain security is the reliance on others. About half of the executives and policymakers surveyed (47%) say their country is moderately or highly dependent on the import of drugs, which illustrates the sheer expanse of the drug production and delivery process.

China and India in particular have become the epicentres of production for the generics and active pharmaceutical ingredients (APIs) that form so much of the industry’s output. Any breakdown in the supply chain here would create serious problems.2

“I think even before the current crisis companies were rethinking their supply chains,” says Roberto Gradnik, a physician and the chief executive of Ixaltis, a biotech start-up. “They were moving away from really extreme globalization.”

Is it the end of an era?

Survey respondents agree with Gradnik. Six in 10 executives (59%) say that the era of offshoring drug manufacturing to low-cost countries is over, and 67% say that the manufacturing of biopharma staples such as biologics would dramatically increase in their own countries over the next three years.

The need to build resilience at home is not just an imperative for countries with a lower GNI per capita. Countries such as Switzerland and the US — among the top five countries for supply chain resilience (see chart 1) — acknowledge that they are vulnerable to scarcity. Figures from the US Food & Drug Administration, for example, show that the US currently has more than 100 drugs in short supply;3 that includes opioid active ingredient morphine sulfate, a key painkiller ingredient, and pindolol tablets used on patients with hypertension.

Chart 1 : Lower GNI per capita countries are fragile on their supply chain

These shortfalls are a concern. And although the Global Biopharma Resilience Index indicates that the biopharma supply chain performs better than other aspects of the industry (see chart 2), there are still a number of areas that need improvement.

The way the industry addresses this weakness will vary from country to country. But increasing domestic production while securing stronger networks with suppliers globally could give it the agility it needs to keep operations running smoothly.

Take Chinese firm WuXi Biologics, for example. With about a decade of experience in the manufacturing portion of the supply chain, the company has rapidly become a key partner for the pharma giants. Dr Chris Chen, WuXi’s chief executive is acutely aware of the risks to global supply chains brought on by Covid-19, but he is of the view that these global bases need reinforcement, while domestic operations are enhanced.

“We are building a very significant facility in Ireland, we have also purchased two facilities in Germany, and we are building a facility in the US,” says Chen. “There will still be a global supply chain. There will be some efforts to build local supply chains but it may not be that easy.”

Martin Meeson, chief executive of Fujifilm Diosynth Biotechnologies, believes that some elements of the supply chain,such as packaging,can benefit from localisation. But he also advocates for stronger global collaboration. “The cost of building a biopharma facility is in the billions,” he says. “And it would certainly not be economically viable for every country to try to put such a facility in place. It would be far more efficient for the world if the level of collaboration that we currently see within the pharma industry is mirrored in the way that the governments interact, in order to use resources efficiently.”

Chart 2 : Much more work is needed to avert a supply chain collapse

The biopharma supply chain on the ground

In a conversation with Adrian van den Hoven, director general of Medicines for Europe, which represents the generic and biosimilars industries, and a closer look at Swiss healthcare giant Roche, we find out how supply chain challenges are playing out in biopharma vs generics, and what industry leaders expect to change in the future.

In conversation with

Adrian van den Hoven

Director general, Medicines for Europe

How do the supply chain challenges faced by the biopharma industry compare with those seen in traditional pharmaceuticals?

Most of the recent issues in supply chain risks and drug shortages relate to traditional (chemical) pharmaceuticals. This is mainly because production of traditional pharmaceuticals is heavily concentrated in a small number of regions — for example specific provinces in India and China — and high levels of consolidation can create risks around security of supply.

But, this is far less of an issue in biopharma supply chains,because biopharma supply chains tend to be more vertically integrated and have more of the production steps centralised in one location, to make them easier to control. Outsourcing parts of biopharma production to other locations is therefore much less common andEurope has invested quite heavily in local biopharma production in recent years.

How are the supply chain challenges likely to change over the next few years?

Biopharmaceutical supply chains have not yet seen the same levels of consolidation as traditional pharma supply chains, but I believe this is likely to happen soon. This is mainly due to the rise of biosimilars, demand for which has been steadily increasing over the past decade.

As with generics, governments are starting to pursue commodity type pricing for biosimilars, to try and get the absolute lowest possible price. This price dynamic started in Europe, and it’s likely to lead to the consolidation of the biopharma production chain within both Europe and Asia. The challenge for governments is that, as well as wanting to lower the cost of biopharmaceuticals, they also want security of supply. In particular, during the pandemic it has been a huge advantage to have certain types of drugs produced in Europe. The dual need for lower prices and security of supply is a difficult challenge for the industry to square.

Which countries are likely to become the biggest exporters of biopharmaceuticals?

At the moment, there are a relatively limited number of countries that are exporting biopharmaceuticals: it is limited to the US, Europe, South Korea and Singapore. However, China and India are getting close to reaching the standards required for exporting biopharmaceuticals — and when this happens there is likely to be a lot of consolidation in the biopharma market.

In my view, there is a much more coherent link between the regulatory process and the manufacturing process in the biopharma industry than in traditional pharma, and this may make it slightly more challenging for China and India to break into the market. We willsee how effective they are in the next couple of years.

A closer look

Building a world-class supply chain at Roche

For Jerry Cacia, the key to navigating supply chain difficulties has been to reinforce industry collaboration.

Roche’s head of global technical development recognises the challenges that have led to increased localisation — “to make sure the supply of critical medicines is secure for each country”.

But like Martin Meeson, Cacia says that this should not cause a total abandonment of the global system. “In some cases, it makes perfect sense to localise manufacturing — parts of your supply chain,” he says. “In other cases I would argue that it does not make sense, because these are very complex processes and frankly the costs will be really high.”

Roche’s success with manufacturing networks, says Cacia, has come from not having the supply chain “purely relegated to a specific country or region” for APIs, but through close relationships with suppliers that act as a pillar of support. It was able to “mobilise very quickly” to join forces with US biotech firm Regeneron, for instance, to support its production of a Covid-19 antibody treatment.4 In a world without global supply chains, this kind of urgent collaboration would be much more difficult.

Find out more about Cytiva